US student housing has shown its strength in recent years, particularly among ‘Power Four’ markets. But could a decline in enrolments spell weaker performance? Christopher Walker reports

The US student housing market is well established, underpinned by robust demand at major universities and consistent occupancy rates. According to NSC Research, in autumn 2025 there were over 19.4m post-secondary enrolments, including 16.2m undergraduate and 3.2m graduate students. With 19.2m students the previous year, this is a 1% increase in total post-secondary enrolment, driven by undergraduate gains of 1.2%.

Yardi Matrix estimated final academic year student housing occupancy at 95.1% in September 2025, up 150bps year on year and the second-highest level since 2019. Autumn 2026 pre-leasing activity began with strong momentum as students continued the trend of securing housing – reaching 47.6% in December 2025, exceeding the 36.8% of December 2024 and 39.6% of September 2023.

Leading the enrolment growth in the US are major public universities. High-growth university markets, particularly those home to ‘Power Four’ schools – universities that make up the top four major athletic conferences, SEC, ACC, Big 10 and Big 12 – are leading the nation in student-housing demand, according to Todd Henderson, head of real estate for the Americas at DWS. At these schools, university-owned housing is often “insufficient, creating demand for off-campus housing units”, he says.

As Henderson sums up: “The US student housing market continues to demonstrate durable fundamentals as it moves through the 2025-2026 leasing cycle.”

However, this mature market is showing some signs of ageing. New bed deliveries slowed to about 22,000 in 2025 from 38,000 in 2024. Henderson attributes this to multiple structural factors: elevated construction costs, lengthened development timelines, and increasing municipal opposition to off-campus housing. Because of this, he says, “development timelines have extended from a typical 18-24 months to 20-30 months depending on size of deal, construction type and location”.

But Michael Erickson, managing director of investments at Greystar, thinks that last point explains it all. “The recent slowdown in new supply is a function of the lagging impacts of capital markets’ volatility seen in late 2022 and beyond. Naturally, the material increases in interest rates significantly lowered the amount of feasible development opportunities.”

Declining enrolment and market bifurcation?

“The number of high school graduates is expected to start falling in 2026, forcing colleges to adapt to a shrinking applicant pool”

Todd Henderson

Nevertheless, the higher education landscape in the US is evolving rapidly. “The number of high school graduates is expected to start falling in 2026, forcing colleges to adapt to a shrinking applicant pool,” says Henderson.

Should investors be worried about this drop? Brett Fawley, director of insights and intelligence at CBRE Investment Management, says: “Obviously, we do not want to build into a market that we expect to have declining enrolment.” But he also thinks that assumption is not set in stone. “Student housing supply and demand is often chicken and egg. Developers build into enrolment growth and universities have more opportunity to grow enrolment [and revenue] when housing availability and cost are not as much of a constraint.”

A decline in enrolments could lead to a market bifurcation. “There will likely be a growing gap between large tier-one institutions with steady enrolment growth and improving student profiles, and smaller public or private institutions, which are struggling to attract students,” says Henderson. “Our view is that power-four markets, flagship public universities and the most elite academic institutions will continue to grow their market share as enrolment growth consolidates.” DWS therefore continues to target these.

Erickson also worries that lower-tier and certain private institutions tend to experience greater enrolment “volatility”. He notes: “While many of these schools are currently benefitting from spillover demand created by increased selectivity at tier-one universities, we apply a more selective approach to development at these campuses.”

Bifurcation may also be the survival strategy for other challenges. While construction costs have moderated from peak levels, Erickson thinks “uncertainty around tariffs, labour availability and municipal requirements continues to complicate underwriting and extend entitlement and delivery timelines.” He also points out that insurance premiums, especially in coastal and Sun Belt markets, have risen sharply, and demographic declines are a risk to demand as select states face declining high school graduate cohorts. These hurdles, he says, are “reinforcing a more disciplined development approach, prioritising flagship public universities”.

Similarly, risks related to international student demand and changes in federal funding under the Donald Trump administration concern Erickson. But he notes: “Universities with selective admissions standards can compensate for potential declines in international enrolment by slightly increasing their acceptance rates, without compromising university quality.” He expects shifts in federal funding to have a more significant impact on lower-quality institutions, which “often lack diversified revenue streams, substantial endowments, and active alumni support, making it much harder for them to offset any reduction in federal aid”.

Maybe the policies of the current US administration are not that negative. Jake Anderson, vicepresident at Heitman, points out that international enrolment also declined during the previous administration, as universities “looked to other channels for enrolment growth”. Moreover, he says: “While research-focused graduate enrolment may decline, these students typically do not reside in purpose-built, off-campus student housing.”

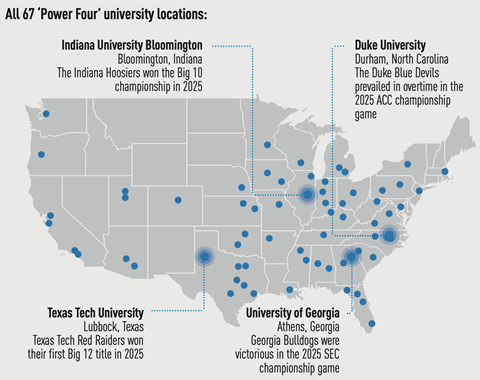

Power Four: Touch down across the US

There are 67 universities spread across the US (see map above) that compete in the ‘Power Four’ athletic conferences in college football.

The conferences include the SEC, ACC, Big 10 and Big 12. Power Four universities have been helping to drive enrolment growth in the US in recent years, leading to an increase in demand for student housing.

The University of Florida, in Gainsville, is represented in the SEC by the Florida Gators (mascots, pictured below). The university had 61,890 enrolments as of fall 2024, up from 60,489 in 2023 and 61,112 in 2021.

19.4m

Number of post-secondary enrolments in autumn 2025, up 1% on 2024

95.1%

Student housing occupancy in final academic year as at September 2025

22,000

New bed deliveries in 2025, down from 38,000 in 2024

Nuance and regional variation

Anderson thinks the largest hurdle for the sector is that development pipelines are beginning to test the depth of demand in some markets. “With only one source of demand, once markets are overbuilt, it is tough to recover,” he says. A bifurcation strategy must therefore be nuanced.

Fawley suggests that strong opportunities exist “off the beaten path”. Like Anderson, he believes that, so far in this cycle, developers have concentrated heavily on a handful of “core” universities – namely, large public flagships in major sports conferences. “As these universities are further built out and the penetration rate rises, developers and their capital will need to cast a wider net beyond the most obvious brand name universities.” This, he says, “may require carefully assessing heightened risks around acceptance rate, prestige, sports conference affiliation, less dynamic local housing markets outside the sunbelt, et cetera”.

Fawley expands on that last point. “In the longer run, the student housing market correlates highly [with] the broader local housing market. Many secondary and tertiary sunbelt markets that host flagship universities have strong overall housing demand drivers beyond the university.” A good example is Knoxville, Tennessee, which has seen a surge in demand and housing costs since 2019. Fawley has “long-term conviction in the demand-side fundamentals of Knoxville but would manage expectations for near-term performance”.

Anderson agrees on the Tennessee example. “Between fall 2025 and fall 2027, the market will see over 8,100 on and off-campus beds, pushing saturation levels to record highs and considerably softening market fundamentals,” he says. He notes that student housing is prone to overbuilding, “particularly in some of the hottest markets”, and every market “requires prudent evaluation of supply and demand trends”.

What is happening in Florida and Texas underscores Anderson’s case for selectivity. “The University of Central Florida and the University of South Florida have historically seen very strong fundamentals and maintained growth, while the University of Florida and Florida State University have indicated plans to slow growth,” he explains. “Similarly, the University of Texas at Austin has long had an enrolment cap, and Texas A&M University has indicated a similar intention to slow growth. We believe this could create opportunities at secondary Texas schools such as Texas State University, Texas Tech University, the University of North Texas, and Sam Houston State University.”

Future outlook

So will bifurcation and selectivity provide a way forward?

Anderson, for one, has not changed Heitman’s target allocations to student housing. “Despite increased investor appetite for student housing exposure, we believe the risks inherent in the sector – large assets in sometimes tertiary locations with a concentrated leasing season dependent on a single source for tenancy (students enrolled at the university) – underscore the need for a price premium relative to conventional multifamily,” he says. Heitman does not typically develop student housing.

But Greystar continues to have conviction in the student-housing sector and believes that student product is an important part of a diversified multifamily housing portfolio. Says Erickson: “Normalising rate growth does not change our favourable view on the sector as long-term investors but does reinforce our belief that proper market selection directly correlates with successful investment outcomes.”

Henderson agrees with this conclusion. “Student housing is well positioned to remain one of the more resilient asset types in real estate, but asset and market selection are paramount to performance. We consider purpose-built student housing an attractive asset class, and it remains an important component of our overall residential investment strategy.”

Student housing: Out of stock?

Higher education is a rapidly growing trillion-dollar global industry. The challenges of meeting student housing demand varies across regions

- 1

- 2

Currently

reading

Currently

reading

US student housing: Athletic asset class

- 4

- 5

- 6

- 7

- 8