The real estate sector leads the field in terms of distress levels among listed companies in Europe as it continues to grapple with high interest rates and financing challenges, the latest Weil European Distress Index reveals.

The latest index results, covering the fourth quarter of 2023 and based on data from more than 3,750 listed companies, show that European corporate distress is deepening amid persistent challenges in profitability and lack of investment.

Falling profitability emerged as the biggest driver of corporate distress in the three months to end-December, marking a shift from previous quarters, Weil's research found. Businesses are struggling with the dual challenge of managing rising costs and sustaining production, exacerbated by the ongoing battle against inflation and high interest rates. Rising input costs will squeeze margins further and put more pressure on corporates’ profitability, the law firm predicts.

In the real estate sector, firms continue to be burdened by high interest rates, falling valuations, elevated energy and construction costs and increasingly expensive financing, according to Weil’s research.

In the residential market, rising interest rates are also impacting housing affordability, softening the outlook for house prices.

Andrew Wilkinson, senior European restructuring partner and co-head of law firm Weil’s London Restructuring practice, said: ‘As the real estate sector takes the lead in distress within Europe, it’s clear that investment hesitancy and rising costs are symptoms of a larger economic malaise. High leverage poses a significant vulnerability in an unforgiving market, where companies confront rising costs against a backdrop of falling valuations.’

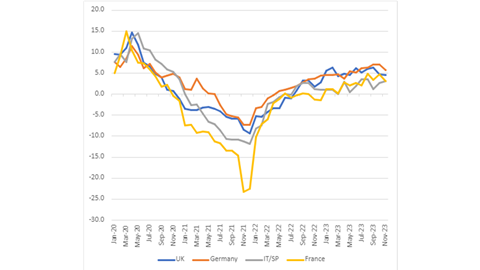

Germany emerges as the most distressed market in Europe, influenced by multiple factors such as deteriorating investment metrics, liquidity pressures and stagnant profitability, which have persisted since the beginning of the year. The country’s economic outlook remains bleak, with both its government and the European Commission projecting a 0.4% contraction in its economy for 2024 due to high inflation, elevated energy prices and sluggish international trade.

Whilst there has been a slight easing of corporate distress in the UK compared to the previous quarter, it remains significantly higher than the same period during the previous year.

Among sectors, healthcare remains the second most distressed as it battles the dual impact of higher interest rates and increasing debt servicing costs.

Neil Devaney, partner and co-head of Weil’s London restructuring practice, added: ‘Corporate distress remains elevated, with profitability at the core of the problem for many companies, as they struggle with increased costs and challenges to supply and production. Though there are some signs of economic improvement, overall distress is at higher levels than this time last year.

‘Recent data reveals GDP declining, and the looming possibility of a recession, across a number of developed economies in Europe. Combined with escalating geo-political tensions and over half of the world’s population heading to the polls in 2024, the path ahead for many businesses remains deeply uncertain.’

Weil defines corporate distress broadly as uncertainty about the fundamental value of financial assets, volatility and increases in perceived risk. It notes there are several common characteristics of corporate distress, such as liquidity pressures, reduced profitability, rising insolvency risk, falling valuations and reduced return on investment.