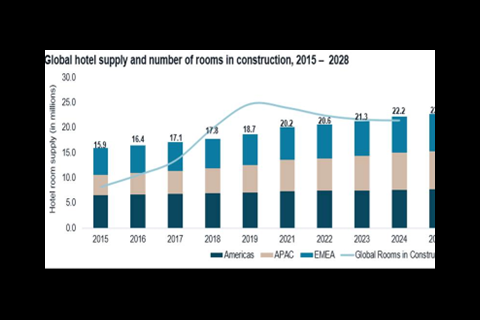

With global supply of new hotel assets expected to be just 2.4% over the next few years due to issues such as higher construction costs, JLL says hotel operators are finding a speedier route to ‘net unit growth’.

JLL’s global head of hotel research, Zacharia (Zach) Demuth – who spent ten years working at Marriott – noted that traditionally 50% of growth and revenue comes from existing hotels while 50% stems from new assets.

‘What we’ve seen is that outside of parts of Asia and the Middle East, new supply – the building of hotels – is close to zero. From the brands’ perspective, they have to look elsewhere.’

The two main options are for a brand to put its ‘flag’ on a hotel when one is bought or sold, or achieve growth via merger and acquisition activity.

Demuth believes it unlikely there will be another m&a transaction any time soon close to the scale of Marriott International’s 2016 acquisition of Starwood Hotels & Resorts Worldwide, which brought together 30 brands and over 5,700 properties.

However, the major brands find themsleves in somewhat of a similar position as they need to acquire other brands in order to grow their portfolios.

Hilton appears to be leading the pack when it comes to m&a.

In March, Hilton put pen to paper on a $210 mln deal for Graduate Hotels from Adventurous Journeys Capital Partners. In April, it acquired a controlling interest in Sydel Group to expand NoMad Hotels from its existing flagship London location to high-end markets around the world. As many as 100 could be developed over time with 10 said to be in advanced talks.

And, just days ago, Hilton announced it was dramatically expanding its portfolio of luxury assets with the addition of 400 boutique properties via a strategic partnership with Small Luxury Hotels of the World (SLH), predominantly in Europe, woith some in the US and southern Asia. Marriott announced a similar partnership with MGM Hotels & Resorts.

Other hotel brands are taking the same approach, though not at the same rate. At the end of June, Hyatt announced the acquisition of Me and All Hotels from Lindner Hotels in Germany – a relatively small deal that will add a 29th brand to Hyatt in a country where it has not had many choices. The German chain has six hotels and a pipeline for extra beds in Berlin, Hamburg, Leipzig, and Stuttgart, and possibly outside of Germany too.

‘We haven’t seen this level of m&a activity from the brands. We have seen it in private equity, and we see it in public real estate. But we haven’t seen this from the brands.’

Limited supply in the last few years is down to covid, the disruption of supply chains and rising construction costs. In addition, the debt markets are not favourable for construction finance.

‘I think a lot of investors have pivoted to acquiring hotels as opposed to building new ones.' added Demuth.

The big four hotel brands – Hilton, Marriott, Hyatt and IHG, plus Accor from Europe – are enjoying balance sheets that are healthier than ever, with significant capital to deploy. Many hotel companies decreased overheads during covid and became asset-light by selling off almost $3 bn of assets that they owned.

JLL employs 370 in its global hotel and hospitality team and has advised on $83 bn of transactions over the past five years. Said Demuth: ‘I can say pretty confidently there will be at least two or three other transactions of note over the remainder of the year and probably some smaller ones that we are not yet aware of.'

Europe

He added that Europe and Asia provided compelling opportunities given the fragmented nature of its markets.

'Europe is up, and we are seeing a lot more investment into European hotels from domestic private equity as well as foreign capital, partly helped by the strength of the dollar.'

PE firms are not just deploying capital to buy assets but are also investing in entire hotel platforms.

In February, investment firm BDT & MSD entered into a strategic partnership with The Friedkin Group to buy a minority stake in Auberge Resorts Collection, which has a portfolio of 27 luxury hotels in the US, Latin America and Europe, and which just opened in London with a second thought to be on the way.