Legislation supporting Europe’s goal of net-zero carbon emissions will make non-compliant commercial buildings almost redundant. As it stands, a vast majority of buildings fall into this category, failing to meet the environmental standards set to be introduced over the coming decade. With Europe’s net-zero commitments in mind, refurbishment – rather than wholesale redevelopment – will be the preferred choice for many investors looking to create environmentally compliant buildings. But completing this task, on this scale, will require massive investment: is the banking sector up to the job?

With buildings alone responsible for 40% of the EU’s carbon emissions, improving their energy efficiency is crucial in the battle to tackle climate change. Key to achieving this are energy-efficiency performance targets, which have been introduced by various European governments. Underlying this approach are energy performance certificates (EPCs), which form a baseline to assess improvements in a building’s energy efficiency. In the UK, from 2023 it will be illegal to let a building with an EPC rating of F or G, and from 2030 it is proposed that this will also be the case for buildings rated C, D and E, with an interim target for buildings to achieve at least a C rating by 2027 to remain compliant. In Europe EPC regimes vary, but, as in the UK, corporate occupiers are driving demand for assets that perform to high EPC standards.

Recent research conducted by CBRE Investment Management’s credit research team estimates that a staggering 60% to 75% of the amount of non-residential real estate stock across Europe is in need of refurbishment if it is to comply with EPC B standard – the legally imposed or adopted minimum standard being set by many European countries from 2030. But to retrofit an existing building to achieve an EPC B rating is no small undertaking. Although the costs of uprating an office with an EPC rating of F or G to B or C varies, Property Market Analysis puts the estimated cost at £200 (€240m) to £300 per sqm.

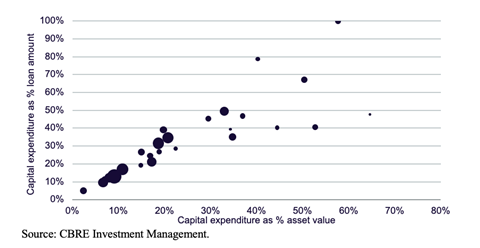

This is a significant cost that goes far beyond standard maintenance and should be considered a one-off major investment expense. According to our sample of 2021 ESG loan requests, the capital expenditure required for ESG-led refurbishment projects, as a proportion of asset value, is typically 15% to 35%, averaging just under 25% – a substantial chunk, as shown in figure 1.

Figure 1: Capital expenditure requirement in ESG-led office refurbishment lending opportunities, 2021

Using various matrices, we have estimated the size of the European commercial real estate market to be €1.2trn. If 60-75% of commercial real estate requires retrofitting to meet ESG standards, the stock of debt this represents is estimated at €720bn to €900bn, of which approximately half will be office buildings. From this we estimate that the credit for capital expenditure needed to bring office buildings up to standard is €360bn to €450bn.

In the past, the banking sector has played an important role in real estate finance. But following the global financial crisis and the subsequent regulation introduced to reduce the risk of another credit crunch, such as Basel IV, capital-requirements regulations and ‘slotting’ in the UK, banks have been encouraged to avoid ‘value-added’ lending. This means that banks alone will not be able to fulfil this new lending demand. Given the massive opportunities of this market and the sheer scale of the finance involved, even set against the aggregate size of banks, non-bank lenders such as private equity funds, insurance and pension funds, will be needed to fill the gap.

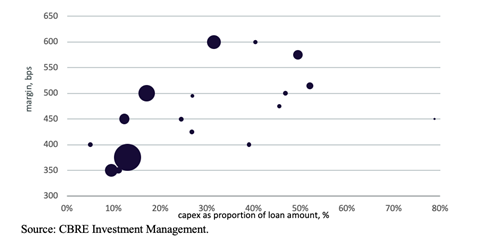

For such lenders, the opportunity presented by ESG-led refurbishment is as big as the need for their offers of credit. Their strong position will allow them to effectively pick and choose the schemes that offer the best margins and strongest location fundamentals. Figure 2 shows that, based on our 2021 pipeline of ESG-led refurbishment projects, it is common for margins to be in the range of 400bps to 500bps, which, when fees and the Bank of England’s SONIA interest-rate benchmark are taken into account, can add up to returns comfortably sitting in the range of 6% to 7%.

Figure 2: Margin versus capital expenditure requirement in ESG-led office refurbishment lending opportunities, 2021

For the market, the shortfall of capital may risk retrofitting being concentrated in the most desirable locations, leaving other less-appealing areas left behind without lettable stock. But for the cohort of lenders who have built capability to meet one of real estate’s most pressing challenges, the opportunity to deliver good returns whilst simultaneously meeting ESG goals will be hard to ignore.